user@devops:~$ cat README.md

Random Forest — Loan Risk Prediction

# Description

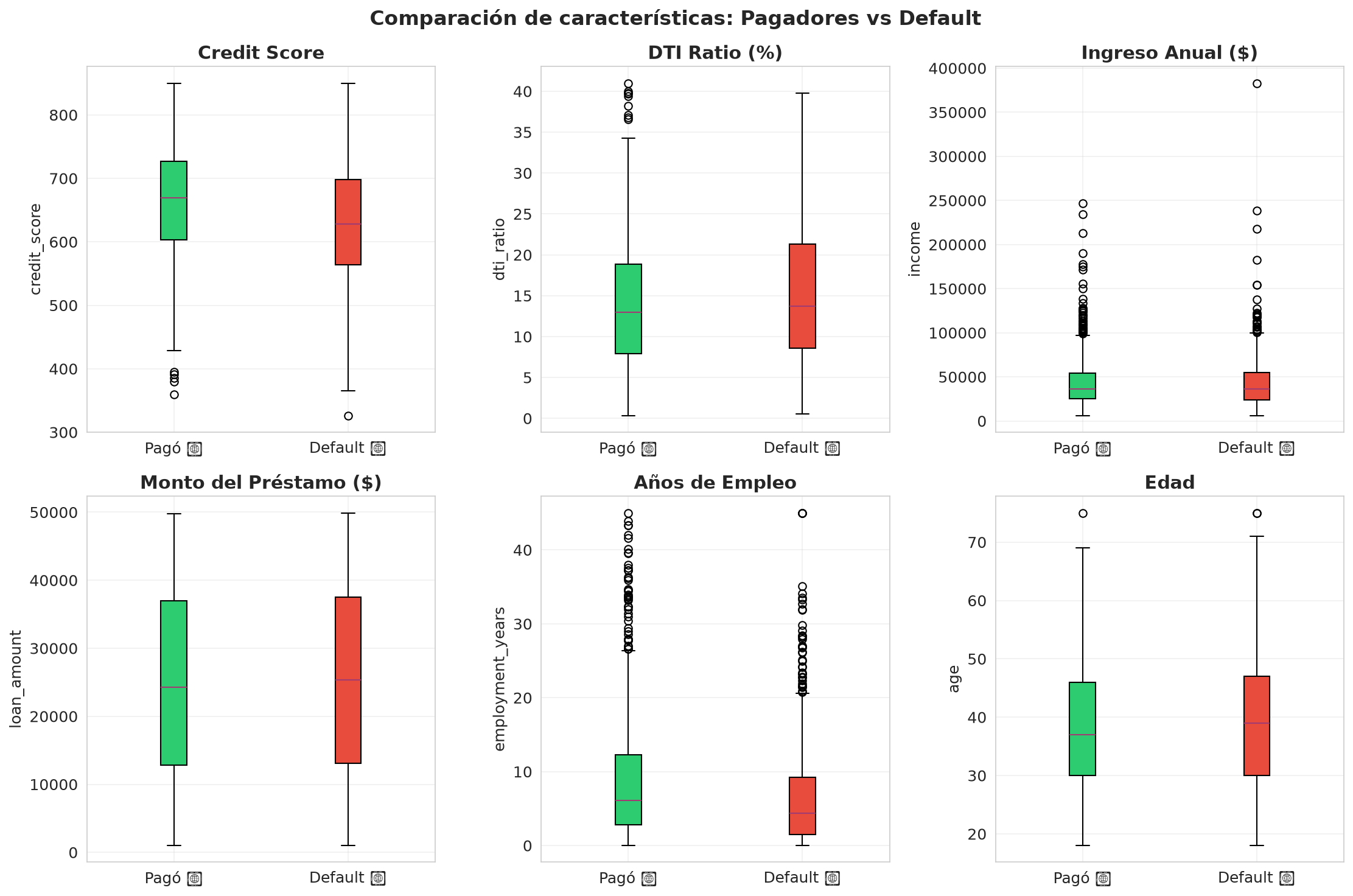

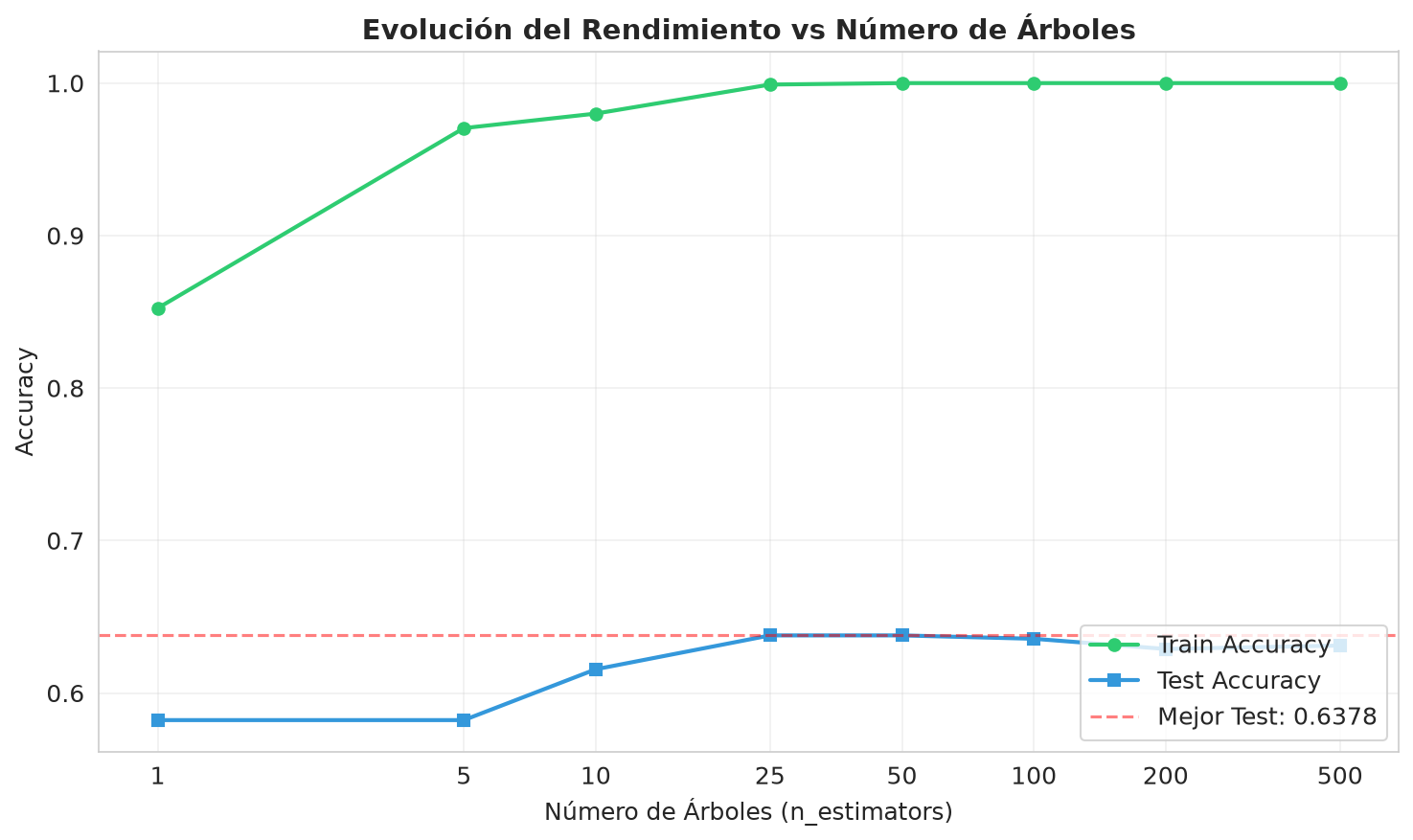

Random Forest project for loan default risk prediction with realistic synthetic data of 1,500 bank customers. Learn how an ensemble of 100 trees outperforms a single decision tree: bootstrap sampling, random feature subsets, and voting aggregation. Compare metrics (accuracy, precision, recall, F1, AUC-ROC), analyze feature importance, tune hyperparameters (n_estimators, max_depth), and visualize ROC curves. Practical demonstration of why 100 voting experts rarely make mistakes.

# Key features

$ Single Tree vs Random Forest comparison with detailed metrics

$ Bootstrap sampling and random feature subsets for diversity

$ Feature importance: credit risk factor ranking

$ ROC curves and AUC for classification evaluation

$ Hyperparameter tuning: n_estimators, max_depth

$ 5-fold cross-validation for robustness

# Gallery

# Technologies used